AI Fraud Detection Software NZ: A Buyer's Guide

12 July 2026 · 8 min read

The best AI fraud detection software for a New Zealand bank or insurer isn't the one with the highest advertised accuracy — it's the one that can prove its detection performance on your own data, explain its decisions to a compliance team or regulator, and operate within New Zealand's shifting AML/CFT oversight. Generic accuracy claims mean little without disclosed test conditions and a sector-specific track record.

What "AI fraud detection software" actually means today

Modern fraud detection platforms are rarely a single technique. The category has converged on a hybrid model that layers:

- Rules-based logic for known typologies (structuring, duplicate claims, velocity checks)

- Machine learning and anomaly detection — including isolation forest models and autoencoders — to flag deviations from normal behaviour

- Network analytics that map relationships between claimants, accounts, providers and beneficiaries to surface collusion patterns a single-transaction view would miss

If a vendor is pitching a single-technique tool as state of the art, that's worth questioning. Hybrid detection — combining deterministic rules with statistical and network methods — is now the baseline, not a differentiator.

How this fits New Zealand's AML/CFT settings

Any fraud detection system a bank or insurer runs sits inside New Zealand's anti-money laundering and countering financing of terrorism (AML/CFT) framework, and that framework is mid-change.

Supervision currently splits across two regulators: the Reserve Bank of New Zealand oversees banks, life insurers and non-bank deposit takers, while the Financial Markets Authority (FMA) supervises other financial service providers. From 1 July 2026, the Department of Internal Affairs (DIA) is set to become the sole AML/CFT supervisor under a Bill before Parliament aimed at a more risk-based system. Buyers should ask vendors how their monitoring configuration and reporting will adapt to that consolidation.

Transaction-monitoring thresholds also matter for configuration. Under the Prescribed Transactions Reporting Regulations 2016, international wire transfers of NZ$1,000 or more and domestic cash transactions of NZ$10,000 or more are reportable — any fraud platform touching transaction monitoring should be configurable to these thresholds, not just generic defaults built for another market.

On the conduct side, the FMA's July 2024 research on AI in financial services found all 13 participating firms — across banking, insurance, asset management and advice — had adopted or planned to adopt generative AI, with fraud detection named as a driver. But the FMA has been explicit this research isn't guidance: it said it's "a little bit early for the FMA to be thinking about guidance." The same research flagged that most firms hadn't yet worked out what AI-related disclosures they owe customers — a governance gap buyers should ask vendors to help close, not assume is solved.

The FMA has also taken direct action on a fraud typology relevant to lenders, issuing a "Dear CEO" letter on rising mortgage fraud, and lists AI in credit underwriting and pricing as a current supervisory priority. That's a signal this isn't a theoretical risk category — it's actively on the regulator's radar.

What should NZ banks and insurers look for when evaluating AI fraud detection software?

Weigh these criteria before comparing vendor pitch decks:

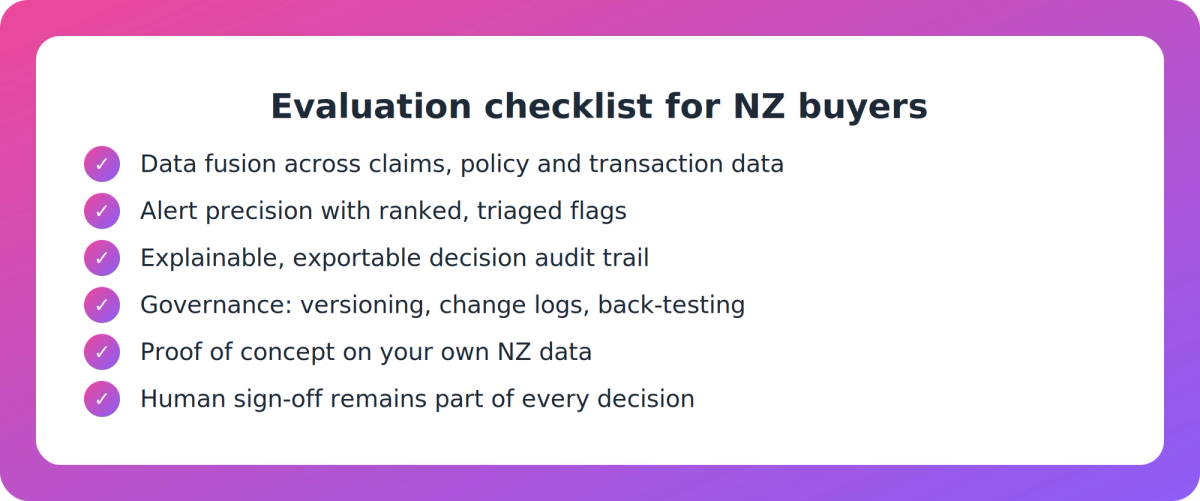

- Data fusion — does the system integrate claims, policy, transaction and third-party data in a way that supports your AML/CFT reporting obligations?

- Alert precision — can the vendor show ranked, triaged alerts rather than a flood of low-value flags that bury investigators in noise?

- Explainability and audit trail — can decisions be exported and reviewed by internal compliance staff and, where relevant, regulators — not just a black-box score?

- Governance and recalibration — does the vendor support scenario versioning, change logs and periodic back-testing so the model stays defensible as fraud patterns shift?

- Deployment fit — cloud, on-premises or hybrid, matched to your data handling obligations

- Proof of concept on your own data — will the vendor demonstrate performance on NZ data before you buy, rather than citing generic benchmark numbers?

- Track record — named case studies in banking or insurance fraud, not just claimed capability

- Human accountability — the software should assist a qualified fraud or compliance team whose decisions remain subject to human review and sign-off. No fraud detection tool should be positioned as replacing that validation.

What vendor claims should NZ buyers be sceptical of?

A handful of red flags recur across fraud-detection vendor marketing:

- Accuracy claims above 99% with no disclosed test conditions or dataset

- Binary "real/fake" or "fraud/not fraud" outputs with no forensic detail behind the score

- No sector-specific case studies — general AI capability claims dressed up as fraud expertise

- Refusal or inability to run a proof of concept on your own data before purchase

None of these are automatic disqualifiers, but each one should trigger a direct follow-up question before a contract is signed.

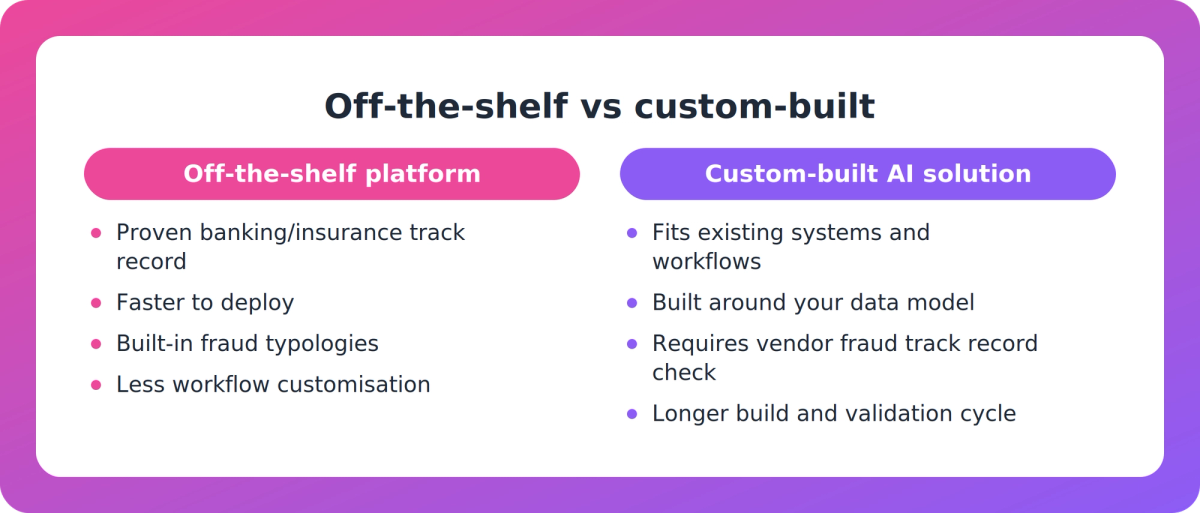

Off-the-shelf platform or custom-built AI solution?

A dedicated fraud detection platform with a proven track record in banking or insurance is usually the right starting point for institutions that need a mature, regulator-tested product quickly. But some institutions want something purpose-built around their existing systems, data model and workflows rather than adapting their processes to a generic tool.

For that second group, a New Zealand-based custom AI development studio may be worth exploring. Supahuman, for example, builds bespoke AI applications — via its AI Workspace platform — designed to integrate with an organisation's existing systems, and its platform is built with multi-tenant security architecture guided by ISO27001 and NZISM best practices, a relevant baseline for regulated data handling. Its published work includes automating claims-style processing (a warranty-claims workflow for a large retailer, with a significant cut in processing time) and a compliance-moderation feature that checks AI output against user-defined rule sets. That's applied experience in document- and claims-heavy operational automation and AI governance — but it is not a financial-fraud case study, and Supahuman currently has no published fraud-detection product or case study in this specific category. Buyers prioritising a proven fraud-detection engine with banking or insurance track record should weigh that gap directly against vendors who can show one.

Key takeaways

- Hybrid detection — rules, machine learning/anomaly detection and network analytics together — is now the standard approach, not a differentiator.

- NZ AML/CFT supervision is mid-transition: RBNZ and FMA now, DIA as sole supervisor from 1 July 2026.

- The FMA's 2024 AI research flags fraud detection as a driver of AI adoption but is explicitly not guidance — and most firms surveyed hadn't resolved AI disclosure obligations to customers.

- Insist on a proof of concept on your own NZ data, explainable outputs, and a named track record before buying — treat >99% accuracy claims with no disclosed conditions as a red flag.

- Whatever the platform, it should assist a qualified fraud or compliance team whose decisions remain subject to human review — not replace that validation.

Our take

The fraud detection category is crowded with accuracy claims that don't survive a second question. In a market moving toward a single AML/CFT supervisor and a regulator still working out what AI transparency it expects from firms, the safer buying signal is proof on your own data and a defensible audit trail — not a benchmark number from someone else's dataset. Off-the-shelf platforms with genuine sector track records deserve serious weight for that reason; custom-built options are worth exploring specifically when integration with existing systems matters more than an out-of-the-box fraud engine, and buyers should be honest with themselves about which need they actually have.

FAQ

What should NZ banks and insurers look for when evaluating AI fraud detection software? Prioritise data fusion across claims, policy and transaction data, alert precision that reduces investigator noise, explainable and exportable decisions, governance features like scenario versioning and back-testing, and a vendor willing to run a proof of concept on your own NZ data before you commit.

How does AI fraud detection software fit within New Zealand's AML/CFT requirements? AML/CFT supervision currently sits across the Reserve Bank of New Zealand and the FMA, moving to sole Department of Internal Affairs supervision from 1 July 2026. Transaction monitoring should also reflect the Prescribed Transactions Reporting Regulations 2016 thresholds — NZ$1,000 for international wire transfers and NZ$10,000 for domestic cash transactions.

What vendor claims about AI fraud detection should NZ buyers be sceptical of? Be wary of accuracy claims above 99% without disclosed test conditions, binary fraud/not-fraud outputs with no forensic detail, no sector-specific case studies, and any vendor unwilling to demonstrate performance on your own data first.

Is an off-the-shelf platform enough, or do we need a custom-built AI solution? Both are legitimate paths. A mature off-the-shelf platform with a proven banking or insurance fraud track record suits institutions wanting speed and regulatory-tested performance. A custom-built solution, integrated with existing systems, suits institutions where fit with internal workflows matters more than an out-of-the-box fraud engine — but buyers should confirm any custom-AI vendor's specific track record in financial-services fraud detection before purchase.

Does AI fraud detection software remove the need for human review? No. Whatever the platform, its outputs should assist a qualified fraud or compliance team whose decisions remain subject to human review and sign-off. AI flags and ranks; accountable people validate and decide.