The Hidden Cost of Manual Data Entry in NZ Finance

13 July 2026 · 8 min read

New Zealand financial services firms report some of the highest AI adoption rates in the world, yet sector productivity fell in 2026 and manual data entry still eats up staff hours. The gap isn't adoption — it's that most firms have bolted AI onto old processes instead of redesigning the compliance-heavy workflows underneath, and the cost of that gap is now showing up in the numbers.

NZ's AI adoption looks good on paper — so why hasn't productivity moved?

Newswire NZ, citing Deloitte research, reported that despite most New Zealand businesses now using AI in some form, productivity actually went backwards in 2026. That's a strange result if AI were doing what the marketing promises — unless the tools are running on top of unchanged processes rather than replacing them.

PwC New Zealand's AI Jobs Barometer adds a specific, sector-level data point: financial services, alongside health and the public sector, saw a decline in AI-related hiring share in recent years — running against the global trend of AI roles growing. That's a signal worth taking seriously. If AI were being embedded structurally into financial services operations, you'd expect hiring patterns to shift toward AI-literate roles, not away from them.

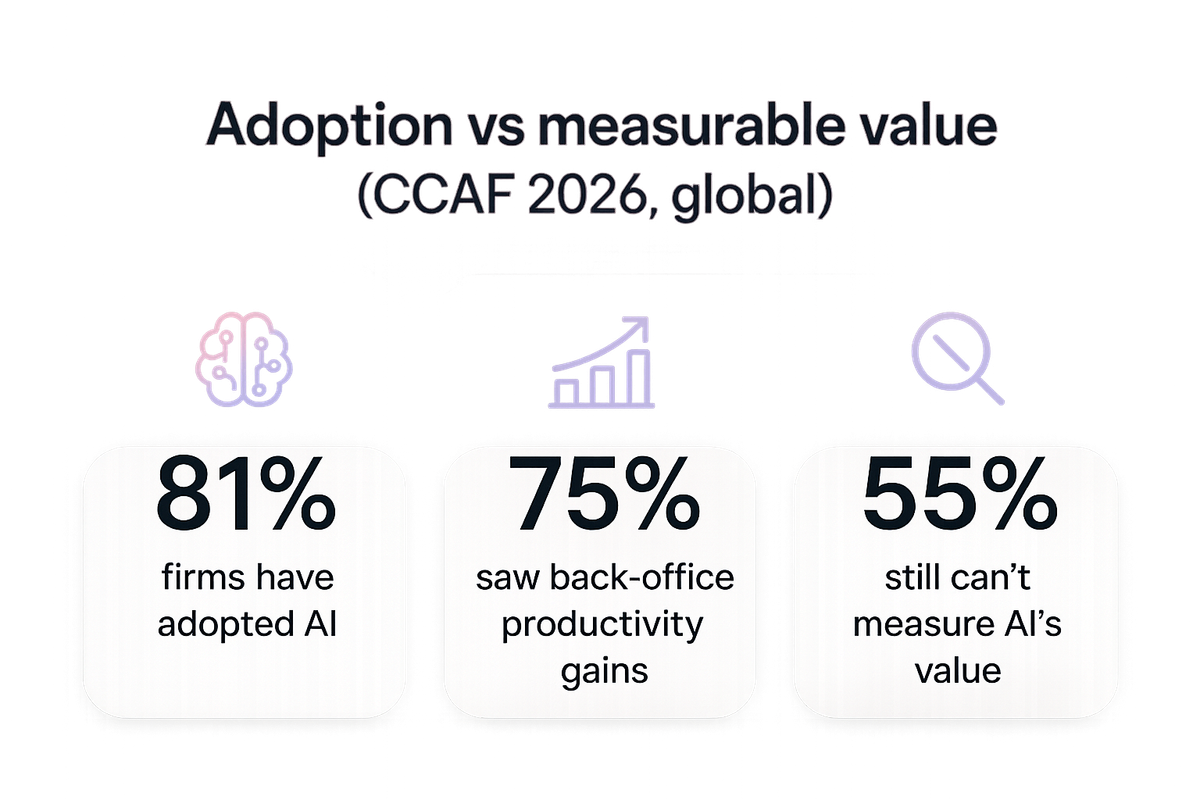

A global comparison point helps make sense of this. The Cambridge Judge Business School and Cambridge Centre for Alternative Finance's 2026 Global AI in Financial Services Report found:

- 81% of financial services firms globally have adopted AI at some level.

- Back-office and operations roles saw the strongest reported productivity gains, at 75%.

- Yet 55% of firms still struggle to measure the actual value of their AI deployments.

That last figure is the tell. High adoption plus a majority unable to measure ROI is exactly what you'd expect from tools switched on without the underlying workflow being rebuilt around them — adoption without redesign.

Where is the manual work still hiding in financial services?

Despite the adoption headlines, a lot of NZ financial services back-office work remains stubbornly manual — particularly the compliance-heavy tasks that don't lend themselves to a generic chatbot bolted onto a legacy system:

- Re-keying client and transaction data between systems that don't talk to each other.

- Manual onboarding, loan origination and KYC document handling.

- Paper-based or semi-digital compliance workflows that still need a human to check, stamp and file.

Industry commentary from automation vendor REGRAVITY (vendor-sourced, so read with appropriate scepticism) estimates manual data entry can cost tens of thousands of dollars per employee per year in lost productive time, with finance staff spending a significant share of the working week simply moving data from one system to another. Whatever the precise figure for any given firm, the direction is consistent with what CFOs and bank commentary are describing: repetitive, compliance-heavy manual work that hasn't gone away just because AI adoption numbers are high.

RNZ's coverage of Kiwibank frames this plainly — repetitive manual "toil" is a cost centre banks are actively trying to strip out, specifically so staff can spend more time on customer-facing work. ItBrief NZ's reporting on AI deployment growth in banking echoes this, pointing to automation targeted at manual onboarding, loan origination and KYC document handling as the areas banks are prioritising.

Why is the open banking deadline raising the stakes?

Open banking obligations are forcing a reckoning that generic AI tools can't quietly sidestep. Kiwibank is required to have compliant systems in place from mid-2026, and itBrief NZ reports that MBIE and the Commerce Commission are being urged to consider whether AI tools handling live client financial data should face the same scrutiny as licensed advisers.

That's a meaningful shift in framing. If regulators start treating AI systems that touch live financial data with adviser-level scrutiny, firms still running manual, paper-based or loosely governed compliance workflows will find it much harder to bolt on an off-the-shelf AI tool and call it done. Auditability, data governance and traceable decision paths move from nice-to-have to baseline requirement.

The CFO dilemma: automate junior work, lose the training ground?

BusinessDesk's Mood of the CFO survey found six in 10 New Zealand CFOs believe AI will hurt the development of future finance leaders, with 60% agreeing that automating junior accounting roles undermines skill-building. That's a direct tension worth naming: manual data entry and reconciliation work has traditionally been where junior finance staff learn how the business actually functions.

This isn't an argument against automating data entry — it's an argument for doing it deliberately. If a firm strips out manual re-keying without rethinking how junior staff build institutional knowledge, it risks solving one problem (wasted hours) while creating another (a thinner talent pipeline). The firms getting this right are the ones redesigning the training pathway alongside the process, not just deleting the manual step.

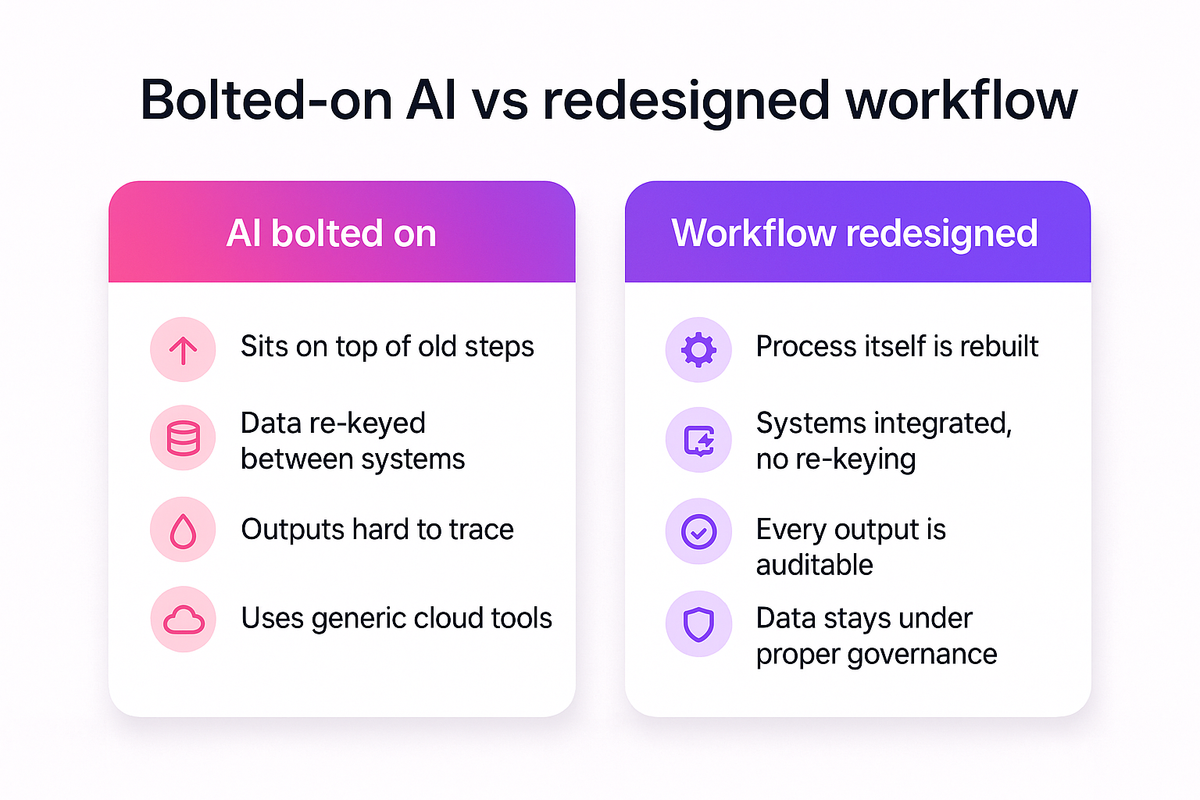

What separates surface-level AI from real workflow redesign?

The pattern across the research is consistent: adoption is high, but structural change is uneven. The firms seeing genuine productivity gains — the 75% reporting back-office improvements in the CCAF study — tend to share a few traits that the "bolted-on" adopters don't:

- Data stays governed. Sensitive client and transaction data runs through systems built for regulated environments, not generic third-party cloud tools.

- The process is redesigned, not just automated. The workflow itself changes — approval chains, document handling, exception routing — rather than AI simply sitting on top of the old steps.

- Outputs are auditable. Every decision or extraction can be traced back, which matters directly for the adviser-level scrutiny now being floated for open banking.

- Integration replaces re-keying. Systems talk to each other, so data entered once doesn't need to be manually copied into the next platform.

Key takeaways

- NZ financial services firms report high AI adoption, but Newswire NZ (citing Deloitte) found sector productivity fell in 2026 — adoption and productivity aren't the same thing.

- PwC's AI Jobs Barometer found financial services, health and the public sector saw declines in AI-related hiring share, against the global trend, hinting at shallow rather than structural adoption.

- Globally, the CCAF's 2026 report found 81% of financial firms have adopted AI and 75% saw back-office productivity gains, but 55% still can't measure the value of their deployment.

- Open banking rules mean Kiwibank must have compliant systems by mid-2026, and itBrief NZ reports calls for AI tools touching live client data to face adviser-level scrutiny.

- BusinessDesk's Mood of the CFO survey found 60% of CFOs worry automating junior finance work will hollow out the talent pipeline — a reason to redesign training alongside automation, not skip it.

Our take

High adoption numbers can mask a real problem: switching on a tool isn't the same as rebuilding the process it sits inside. For NZ financial services, the compliance-heavy nature of the work means the manual steps that survive AI adoption are usually the ones that matter most — client data handling, onboarding, KYC — precisely the areas open banking scrutiny is about to focus on. Firms that treat automation as a bolt-on will keep re-keying data and keep failing to show ROI; firms that redesign the workflow, keep data governed, and rethink how junior staff learn the business alongside it will be the ones the productivity gains actually show up for.

FAQ

Why is NZ financial services productivity falling despite high AI adoption? Newswire NZ, citing Deloitte research, reported that productivity fell in 2026 even as most New Zealand businesses reported using AI. The gap suggests many firms have switched AI tools on without redesigning the underlying processes, so manual, compliance-heavy work continues alongside the new tools rather than being replaced by them.

What does the open banking deadline mean for AI use in NZ banking? Kiwibank must have compliant open banking systems in place from mid-2026. ItBrief NZ reports that MBIE and the Commerce Commission are being urged to consider whether AI tools handling live client financial data should face scrutiny similar to that applied to licensed advisers, raising the bar for auditability and governance.

Are NZ CFOs worried about automating junior finance roles? Yes. BusinessDesk's Mood of the CFO survey found six in 10 New Zealand CFOs believe AI will hurt the development of future finance leaders, with 60% agreeing that automating junior accounting work undermines skill-building, since manual tasks have traditionally been where junior staff learn the business.

How much does manual data entry actually cost financial services firms? Industry commentary from automation vendor REGRAVITY estimates manual data entry can cost tens of thousands of dollars per employee per year in lost productive time. This is vendor-sourced commentary rather than independent research, but it's consistent with broader reporting on manual "toil" in NZ banking back-office functions.

What's the difference between AI adoption and real productivity gains in finance? The CCAF's 2026 Global AI in Financial Services Report found 81% of firms have adopted AI and 75% saw back-office productivity gains, yet 55% still struggle to measure the value of their deployment. Real gains tend to come from firms that redesign workflows and keep data governed, not just those that add a tool on top.